We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Oct 29, 2019 / News

Accessing the Producer Rebate on Museum Stock

From 1 July 2018, to qualify for the WET producer rebate on assessable dealings of wine, a producer must meet new eligibility criteria.

There are separate criteria for:

- 2018 and later vintage wines, and

- 2017 and earlier vintage ‘Museum stock’ wines

For Museum stock sold on or after 1 July 2018, a producer will not be subject to the 85% Ownership requirement if all the following apply:

- The producer of wine owned the wine immediately before 1 January 2018, and continued to own it until the assessable dealing (usually sale); and

- The wine was

- i. bottled on or before 30 June 2018, or

- ii. labelled with a vintage date as being 2017 or earlier year; and

- The assessable dealing occurs on or before 30 June 2023.

All assessable dealings of Museum stock or sparkling wines made from 1 July 2023 will need to satisfy all the new eligibility criteria including the 85% Ownership requirement. This will make it difficult for some producers to claim the producer rebate on such wine dealings as they will need to have sufficient documentary evidence that they owned the source product used to make the wine prior to crushing.

The main producers of Museum stock who will be affected include:

- Small to medium sized producers who meet the eligibility criteria to claim the producer rebate in 2018 and later vintages and have annual taxable dealings of less than $1,206,897

- Producers who blend wines and bought fruit juice rather than the fruit from other growers (or other related entities)

- Producers who haven’t maintained written records of the source product quantities making up each Museum stock vintage and batch of wine produced

If you are a producer of Museum stock you need to determine whether or not you will meet all the criteria from 1 July 2023, and if you don’t, ensure that your mark-ups (marked-up price) are sufficient enough to cover the lost producer rebate as well as the additional storage costs incurred over the years the wine is held.

*New Eligibility Criteria

1. Must be the producer of the wine; and

2. Packaging requirement – wine must be:

- packaged in a container of 5 litres or less,

- branded with a trademark owned by the entity (or an associated entity); and

3. WET payment requirement - There must be a WET liability for the assessable dealing, or the purchaser of the wine issues a quote to the producer stating they intend to make a taxable dealing with the wine; and

4. 85% ownership of source product requirement – producer must own at least 85% of the source product used to make the wine at all times, from immediately prior to crushing, right through to packaging.

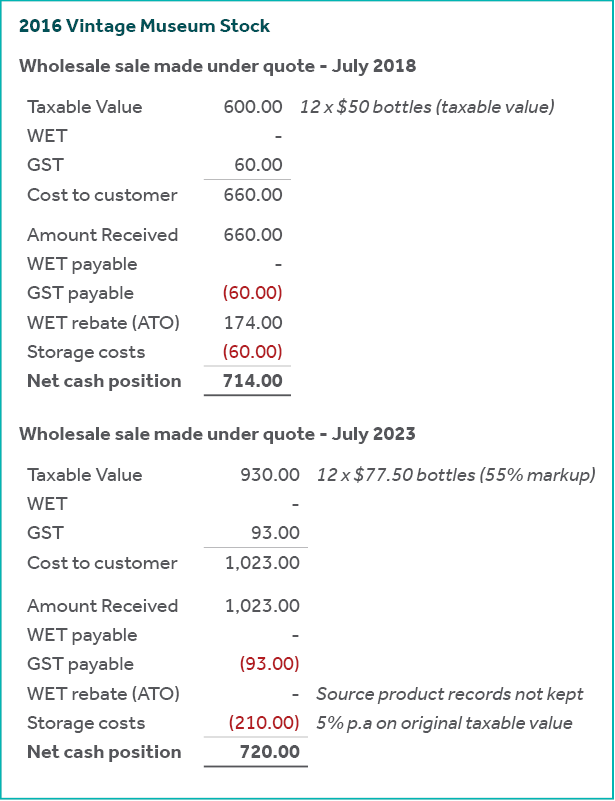

Example

A small wine producer has 2016 Museum stock on hand and doesn’t have records of the source product making up the vintage. They want to know whether they are eligible to claim the producer rebate, and if not, how much markup is required to break even with if they were eligible.

Facts

- Original taxable value per bottle is $50 (excluding WET and GST)

- Producer meets all the eligibility criteria, except the 85% Ownership requirement

1 July 2018 to 30 June 2023

- Producer eligible to claim the producer rebate

- If the producer sells a dozen bottles of the 2016 vintage in July 2018, their net cash position would be $714

1 July 2023 – onwards

- Producer is not eligible to claim the producer rebate

- If the producer sells a dozen bottles of the 2016 vintage in July 2023, they would need to mark up their wine by approximately 55% to break even with previous sales made in July 2018

- The rebate lost in this example would be $269.70 ($930 x 29%)

How can Nexia Edwards Marshall help you?

Please contact George Papanicolaou or your Nexia Edwards Marshall Advisor who will be able to assist you check your eligibility to claim the producer rebate on Museum stock as well as assist identify strategies which can be implemented early including considering tax planning, cash flow forecasts as well as marketing and promotion opportunities.

The material contained in this publication is for general information purposes only and does not constitute professional advice or recommendation from Nexia Edwards Marshall. Regarding any situation or circumstance, specific professional advice should be sought on any particular matter by contacting your Nexia Edwards Marshall Adviser.