We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

May 18, 2022 / News

Accounting for R&D Tax Incentives

The Research and Development Tax Incentive (“R&DTI”) offers tax offsets for entities conducting eligible research and development (“R&D”) activities. Changes to the R&DTI scheme from 1 July 2021 raises questions on the accounting for these incentives.

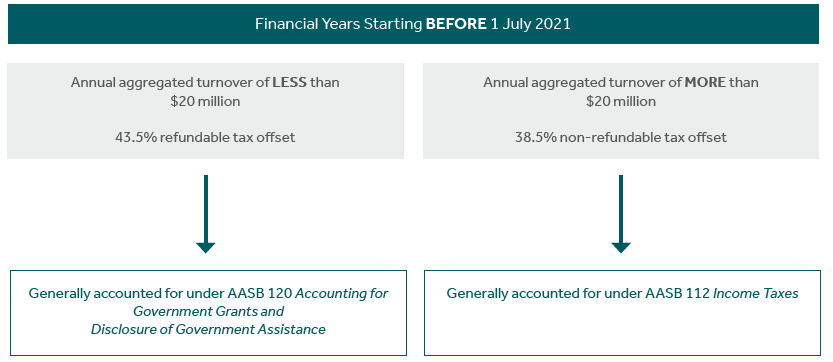

Accounting for R&DTI before 1 July 2021

The accounting treatment varied on whether the tax offset was a refundable or non-refundable tax offset. Deciding if it was refundable or not depended on the entity’s annual aggregated turnover.

An entity was entitled to a 43.5% refundable tax offset for its eligible R&D expenditure if its aggregated turnover was equal to or less than $20 million. Entitlement to the tax offset was not based on the entity’s taxable profit or income tax liability.

Consequently, the offset did not form part of ‘income tax’, which for the purpose of AASB 112 ‘include all domestic and foreign taxes which are based on taxable profits’. Rather, these amounts were a form of government grant because they represent government assistance that are not ‘available in determining taxable profit or tax loss, or are determined or limited on the basis of income tax liability’.

In other words, the claimant was receiving assistance from the government in the form of a refundable tax offset in return for compliance with certain conditions (i.e. eligible R&D expenditure). Therefore, the applicable accounting standard to account for these incentives was AASB 120 Accounting for Government Grants and Disclosure of Government Assistance.

On the other hand, if the entity’s annual aggregated turnover was more than $20 million, a 38.5% non-refundable tax offset applied to eligible R&D expenditure. These incentives could only be used to offset current year income tax payable and unused credits could be carried forward to reduce income tax payable in future financial years. Because these incentives were linked and limited to the entity’s taxable income, these were accounted for as income tax credits under AASB 112 Income Taxes.

This accounting treatment can be summarised in Diagram 1 below.

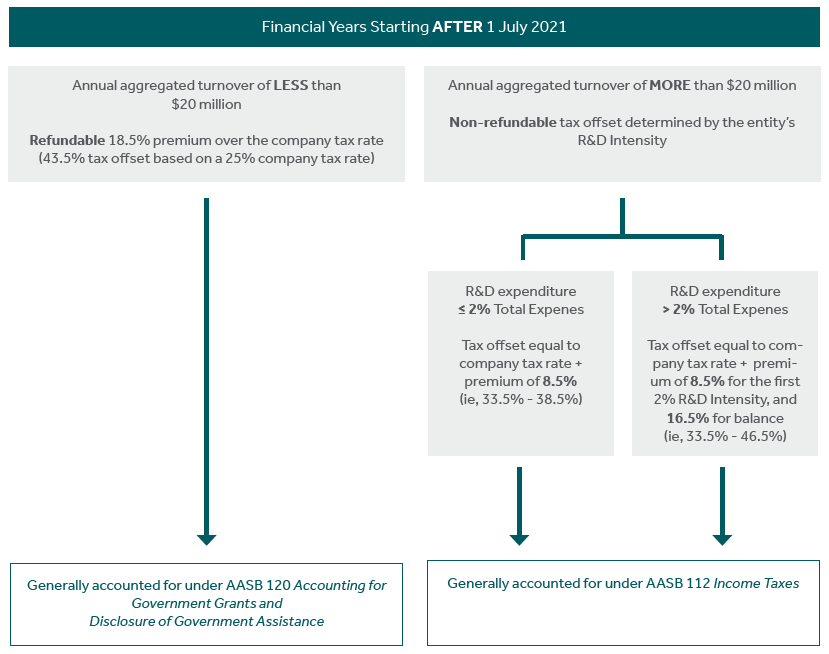

What’s changing from 1 July 2021?

Claiming R&DTI is still dependent on the eligibility of the R&D expenditure as well as the entity’s aggregate annual turnover.

For entities with an annual aggregate turnover of less than $20 million, a refundable tax offset is set at a 18.5% premium to the applicable company tax rate. Hence, a 43.5% refundable tax offset rate will apply for those ‘base rate entities’ eligible for a 25% corporate tax rate.

However, for companies with an annual aggregate turnover of more than $20 million, a key change is the introduction of different R&DTI non-refundable tax offset rates based on the entity’s R&D Intensity. An entity’s R&D Intensity is the percentage of eligible R&D expenditure to its total adjusted expenditure.

If the R&D Intensity is less than or equal to 2%, the R&DTI is an 8.5% premium over the company’s tax rate. If the R&D Intensity is more than 2%, the entity will receive a stepped non-refundable tax offset at 8.5% above the company tax rate on R&D expenditure up to 2% R&D Intensity, then an offset at 16.5% above the company tax rate on R&D expenditure that exceeds this 2% R&D Intensity. The applicable company tax rate is either 25% for a company that is a ‘base rate entity’ or 30% otherwise. This means that the tax offset can range from 33.5% to 46.5%, depending on the applicable company tax rate and the company’s R&D intensity.

Other changes include what qualifies as eligible R&D expenditure, caps on the total amount of eligible R&D expenditure, and determining total expenses. For more information on all the changes, you should speak with your local Nexia R&D tax advisor. In this article, we are focussed only on the accounting implications for R&DTIs.

How will the R&DTI be accounted for after 1 July 2021?

Refundable tax offsets

An entity’s entitlement to the refundable R&DTI is determined by an entity’s turnover and its eligible R&D expenditure. Entitlement to the refundable tax offset is not based on an entity’s taxable profit or income tax liability.

Consequently, for the same reasons as above, the offset does not form part of income tax and the R&D tax offset remains out of scope of AASB 112.

Refundable R&D tax offsets should continue to be accounted for under AASB 120. Therefore, the credit is recognised in profit before tax to match the benefit with the costs for which it is intended to compensate. Companies should determine its accounting policies for the presentation of government grant income (i.e. gross basis or net basis) in its financial report.

Non-refundable tax offsets

In contrast to refundable tax offsets, the non-refundable R&DTI adjusts the entity’s current tax payable where annual aggregate turnover is more than $20 million. To the extent that the tax offset exceeds current tax, the entity is not entitled to receive a refund of those excess credits.

Because the amount of the R&DTI offset is determined or limited on the basis of its income tax liability, it is excluded from the scope of AASB 120. As a result, the non-refundable R&D tax offset should continue to be accounted for under AASB 112.

The accounting treatment for R&DTI for financial years starting from 1 July 2021 can be summarised in Diagram 2 below.

The material contained in this publication is for general information purposes only and does not constitute professional advice or recommendation from Nexia Edwards Marshall. Regarding any situation or circumstance, specific professional advice should be sought on any particular matter by contacting your Nexia Edwards Marshall Adviser.