We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Jul 26, 2021 / News

Accounting Update | Simplified Disclosures Tier 2 Financial Reports

From 1 July 2021, the Tier 2 Reduced Disclosure Regime is replaced by a new Simplified Disclosures Standard. This publication compares the two disclosure standards and explores how transition choices affect the disclosures.

What is changing?

The Tier 2 Reduced Disclosure Regime (“RDR”) is being replaced with a new Tier 2 Simplified Disclosure Standard (“SDS”) which is contained in AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities.

Which entities are affected by this change?

SDS will mandatorily apply to any for-profit or not-for-profit entity preparing Tier 2 general purpose financial statements for annual reporting periods beginning on or after 1 July 2021.

This means that for entities with a 30 June balance date SDS will apply to the financial year ended 30 June 2022, and to the financial year ended 31 December 2022 for those entities with a 31 December balance date. Entities can elect to early adopt SDS.

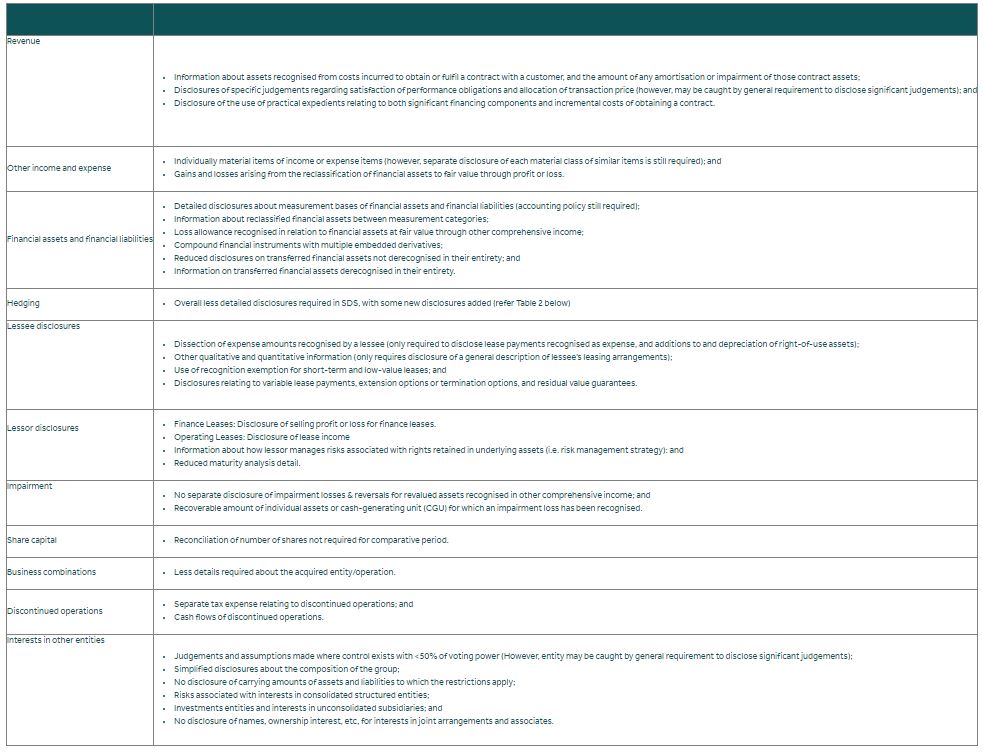

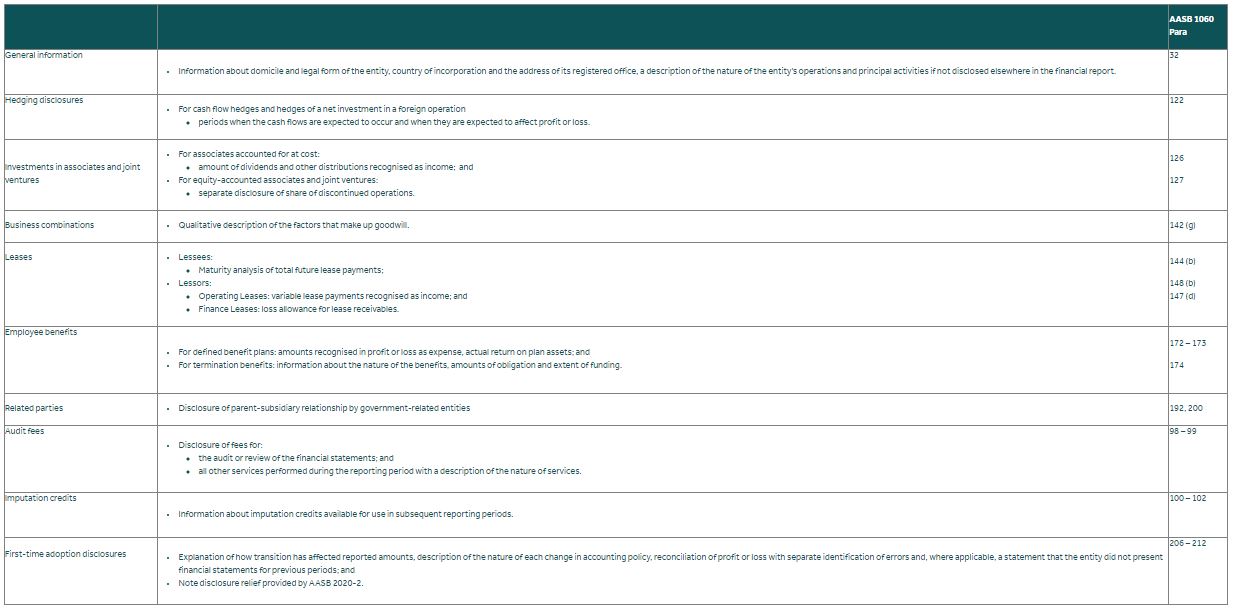

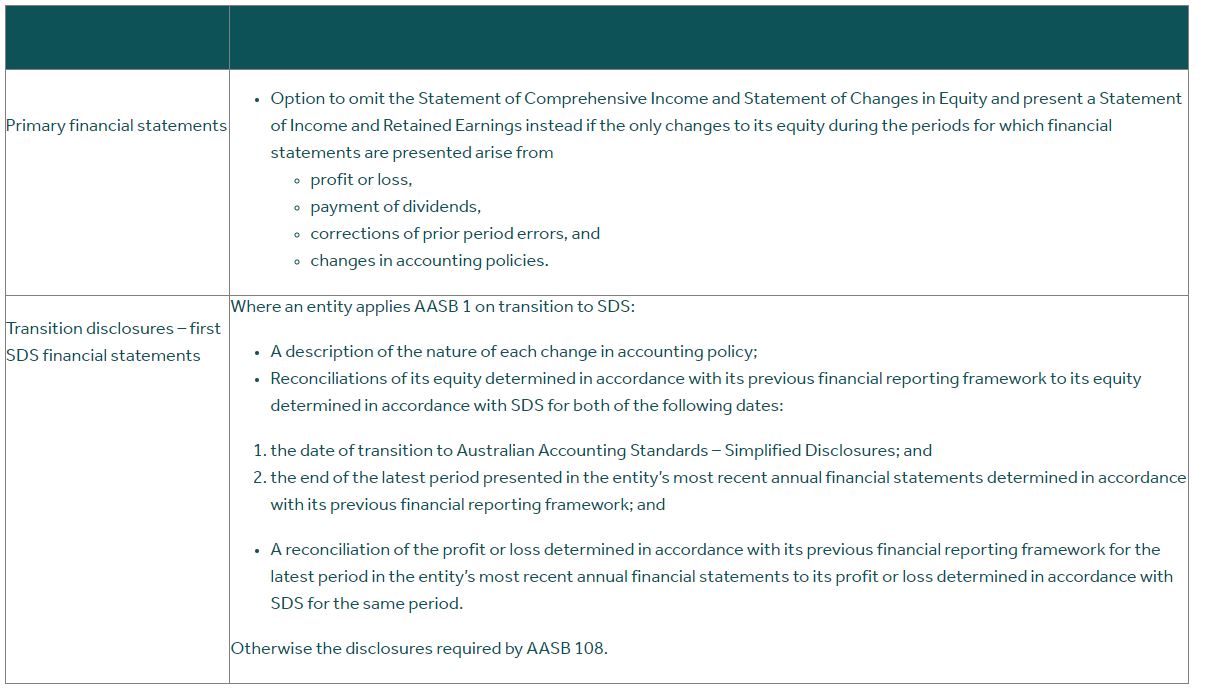

What are the differences between the RDR and SDS disclosures?

The following sections describe the key disclosure changes between RDR and SDS:

Table 1: RDR disclosures reduced by SDS

Table 2: New SDS disclosures not required by RDR

Table 3: Other SDS disclosure changes

Transition choices and disclosures

The application of the various transitional provisions can be complex and depends on a number of factors. This includes whether an entity is for-profit or not-for-profit; whether the entity previously prepared RDR financial statements; and whether AASB 1 or AASB 108 is applied on transition.

An entity can only apply AASB 1 if:

- The entity’s previous SPFS did not comply with all the recognition and measurement requirements of all Australian Accounting Standards; or

- The entity’s previous SPFS were prepared on a stand-alone basis and were not consolidated because the entity (or group) was not considered to be a reporting entity.

In addition, for periods beginning before 1 July 2022 (which includes the first year of mandatory adoption), these entities are not required to distinguish between the correction of errors and changes in accounting policies if the entity becomes aware of errors made in its previous SPFS.

Early adoption of SDS before the mandatory application date

For-profit entities

If a for-profit entity transitions from Special Purpose Financial Statements (“SPFS”) to SDS before the mandatory application date:

- The date of transition is the start of the current financial year;

- It is not required to restate their SPFS comparative financial information to comply with all measurement and recognition requirements of Australian Accounting Standards. This means the comparative financial information is prepared in accordance with the entity’s previous SPFS accounting policies;

- Any accounting policy changes are recognised as adjustments at the start of current financial year;

- It is not required to distinguish between the correction of error and changes in accounting policies if the entity becomes aware of errors made in its most recent previous SPFS;

- Disclosure of any adjustments arising from accounting policy changes on transition is required.

- Additional transition disclosures may apply depending on whether the entity applies AASB 1 or AASB 108 on transition from SPFS to SDS – refer Table 3 above.

A for-profit entity that transitions from RDR financial statements to SDS before the mandatory application date:

- Applies the SDS disclosures to the current and comparative period; but

- Is not required to disclose comparative information for SDS disclosures not previously required by RDR – refer Table 2 above; and

- It is not required to distinguish between the correction of error and changes in accounting policies if the entity becomes aware of errors made in its most recent previous SPFS.

Not-for-profit entities

There is no specific relief for a not-for-profit entity that transitions from SPFS to SDS before the mandatory application date. Hence:

- The date of transition is the start of the previous comparative financial year;

- It is required to restate their SPFS comparative financial information to comply with all measurement and recognition requirements of Australian Accounting Standards;

- Any accounting policy changes are recognised as adjustments at the start of the previous financial year;

- Additional transition disclosures may apply depending on whether the entity applies AASB 1 or AASB 108 on transition from SPFS to SDS – refer Table 3 above.

A not-for-profit entity that transitions from RDR financial statements to SDS before the mandatory application date:

- Applies the SDS disclosures to the current and comparative period; but

- Is not required to disclose comparative information for SDS disclosures not previously required by RDR – refer Table 2 above.

Adoption of SDS at the mandatory application date

Other the limited relief in relation to distinguishing the correction of errors and changes in accounting policies for for-profit entities, no transition disclosure relief applies to either for-profit entities or not-for-profit entities transitioning from either SPFS or RDR to SDS. SDS disclosures will be required for both the current and comparative reporting periods.

Additional transition disclosures may apply depending on whether the entity applies AASB 1 or AASB 108 on transition from SPFS to SDS – refer Table 3.

If you require assistance preparing for these changes, or for any further information, please contact your Nexia Edwards Marshall Advisor.