We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Apr 18, 2019 / News

Possible Abolition of Excess Franking Credits Refunds

With a Federal election due by the end of May this year, and the Coalition Party behind in the polls, the Labor Party’s (ALP) policy to abolish the refund of excess dividend franking credits for many taxpayers, including many SMSFs, is a topic of great interest. To help demystify the topic a little we have outlined the history of dividend franking in Australia and detailed the ALP’s proposal.

History of Dividend Franking

Until 1987 Australia followed what is often called the “classical” model of taxing company dividends. Under this model, companies paid tax on their profits and paid dividends from after-tax profits to shareholders, who in turn paid tax on their dividends with no reference to tax paid by the company. In 1987 the Hawke Government introduced a system of dividend franking, under which tax paid by the company could be applied against tax payable by the shareholder. The aim was to eliminate double taxation, and the franking credit could be applied to reduce the tax payable by the shareholder to nil but did not result in a tax refund.

In 2000 the Howard Government extended the imputation system by allowing franking credits in excess of the tax payable by individuals and super funds such that the credits could generate a tax refund. The availability of excess credit refunds has grown to be a major factor in investment selection and tax planning for many Australians.

The Labor Party’s Policy

The Labor Party proposes to abolish refunds for excess franking credits with effect from 1 July 2019, subject to certain exceptions. The most important exception is what Labor refers to as the Pensioner Guarantee, under which excess franking credit refunds will continue to be available for:

every individual recipient of an Australian Government pension or allowance, including the Age Pension, Disability Support Pension, Carer Payment, Parenting Payment, Newstart and Sickness Allowance, and

every SMSF with at least one member who is a recipient of an Australian Government pension or allowance as at 28 March 2018 (the date of the ALP’s announcement).

Also, charities which are exempt from income tax and not-for-profit institutions with deductible gift recipient status will continue to be entitled to excess franking credit refunds.

The Debate

From the point of view of the Federal Budget, the refund of excess franking credits represents a hole in the revenue “bucket”. It can be viewed, in effect, as collecting tax from companies then giving it away to shareholders. The ALP’s policy announcement claims that these refunds now total $6 billion a year. Of course, the proposal is controversial because, since the introduction of the refunds in 2000, dividend franking refunds have come to be a major investment consideration. Many retirees may depend on these refunds to provide a valuable source of income in their retirement.

There have been conflicting claims over who would be affected by the change. The Coalition has used taxable income data to argue that the change will affect people on low incomes, but this analysis has been criticised on the basis that superannuation pensions paid to people over 60 are not included in taxable income, so potentially large sources of income are being ignored. The ALP claims that its distributional analysis shows that excess franking credits overwhelmingly favour the wealthiest retirees. However, there may be a large number of taxpayers in receipt of smaller amounts who resent the attempt to remove the refunds.

Internationally, there are four other OECD countries with a dividend imputation system similar to Australia’s original 1987 model, but it seems that Australia is alone in allowing the full refund of excess imputation credits.

We may see companies with large franking account balances adopting strategies such as share buy-backs or the payment of special dividends in order to pass on franking credits to shareholders before 1 July 2019.

The ALP has also proposed a number of other significant changes to superannuation, which should not be overlooked, including:

- lowering the non-concessional contributions cap to $75,000

- removing the ability to catch up unused concessional contributions caps over 5 years, and

- removing the deductibility of personal contributions for people who derive mainly salary or wages.

- elimination of limited recourse borrowing arrangements in SMSFs.

The rules relating to superannuation, and in particular SMSF’s, have in recent years been subject to frequent changes, and 2019 looks to be no different. Of course, these changes may take some time to come into effect, so whilst it is good to have an understanding of the proposed changes it is wise to remember that they are currently only proposed and not yet law. Please feel free to contact one of our superannuation specialists if you would like to know any more about the proposed policies

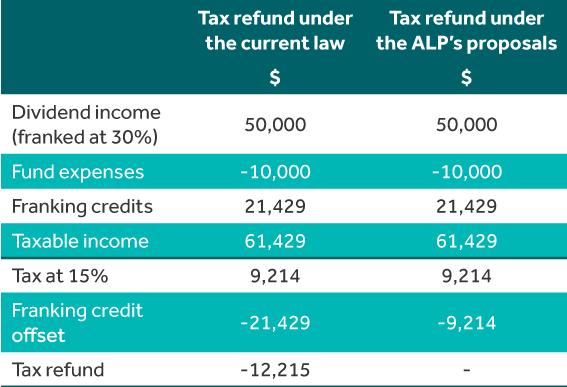

Case Study

The Hopeful Super Fund is an SMSF which has decided to invest heavily in shares paying fully franked dividends, with the aim of taking advantage of the refund of franking credits. All members of the Fund are currently in accumulation phase, and no member is in receipt of an Australian Government pension of allowance.

We compare the Fund’s income tax position under the current law and under the ALP’s proposal below, which would see a return to the original 1987 imputation system.

How can Nexia Edwards Marshall help you?

For any questions or to discuss any of the above in relation to your personal situation, please contact Alanah Boylon or your Nexia Edwards Marshall Adviser.

The material contained in this publication is for general information purposes only and does not constitute professional advice or recommendation from Nexia Edwards Marshall. Regarding any situation or circumstance, specific professional advice should be sought on any particular matter by contacting your Nexia Edwards Marshall Adviser.