We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Apr 17, 2019 / News

The new Revenue standard - It’s 10 minutes to midnight!

Looking back, we first started discussing the new revenue accounting standard, AASB 15 Revenue from Contracts with Customers, in 2014. That seems a long time ago, not helped by the fact that the original application date AASB 15 was deferred by one year, and by another year for not-for-profit entities. For entities that put AASB 15 into the ‘next year’s problem’ file the wait is now over and the standard mandatorily applies to for-profit entities for annual reporting periods beginning on or after 1 January 2018 and for not-for-profit entities from 1 January 2019. That means for-profit entities with a 30 June year end must apply AASB 15 in their 30 June 2019 financial statements.

Not-for-profit entities have to navigate not only AASB 15 but also AASB 1058 Income of Not-for-Profit Entities. One of the biggest practical challenges for our NFP clients to resolve is whether an income stream should be accounted for in accordance with AASB 1058 or AASB 15.

Entities cannot assume that the new standards will have no significant impact. In their Media Release MR 18-364 ASIC also reminded companies that have not already done so should determine the extent of any impact. ASIC noted that the new standards can have real business impacts (e.g, compliance with debt covenants or regulatory financial condition requirements, tax liabilities, dividend paying capacity, and remuneration schemes) as well as the need to implement new systems and processes.

Directors must have a reasonable basis to determine any potential effects of the new standards on the timing and amount of revenue recognition. This can only be done by undertaking a diagnostic and implementation process including:

- Identification and scoping of key income streams;

- Identification of the various types of customer contracts, including obtaining comfort over completeness of different arrangements that exist;

- Documenting Management’s analysis, decisions, rationale and conclusions regarding transition options, exceptions, key estimates and judgements; and

- Management’s assessment and calculation of materiality to determine whether any adjustments on transition are necessary.

The new revenue model

Under the new model revenue is recognise when (or as) the entity satisfies a performance obligation by transferring a promised good or service to a customer at an amount the entity expects to be entitled in exchange for those goods or services.

While the above principle sounds straightforward, it does raise a number of important application issues. For example:

- Does your arrangements with your customers satisfy the definition of ‘contract’ under the new rules?

- What are, and how many, performance obligations exist in your contracts with customers?

- How is the consideration to be measured?

- How is the consideration expected to be received under the contract allocated to multiple performance obligations?

Implementation issues abound

The potential impacts will vary from industry to industry and entity to entity depending upon the nature and source of income and the particular terms of the arrangements with your customers.

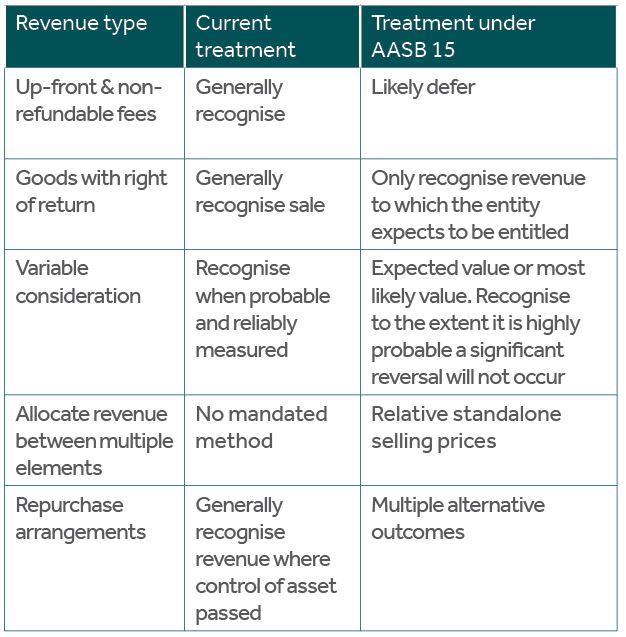

Some examples of potential changes to current accounting practice include:

The above list is by no means comprehensive and other income types may also be affected by the new rules. Some other areas where we have encountered practical challenges, each of which have their own implications and effects on the amount and timing for revenue recognition, are in relation to:

- Assessing whether modifications or changes to a contract should be accounted for separately or as an adjustment to the initial contract;

- Accounting for bundled arrangements;

- Identification of the performance obligation(s) in the contract;

- Determining the appropriate method of measuring progress towards the complete satisfaction of that performance obligation;

- Accounting for rebates, discounts and tiered pricing structures and payments by the supplier to the customer.

The list goes on.

Not-for-profit entities will face their own challenges in applying AASB 15. Applying the new model will require a renewed focus on identifying what are a not-for-profit entity’s performance obligations to transfer a promised good or service to a customer. This is particularly relevant for the receipt of grants, some forms of donations and other contributions, as well as up-front fees.

Are you prepared?

The new revenue standard has the potential to impact a wide range of revenue types and industries. The introduction of the new requirements has the potential to have wider implication than just accounting. It has the potential to affect areas dependent upon revenue measures such as:

- covenant calculations,

- future earn-outs in business combinations,

- employee bonus schemes, and

- deferred tax consequences,

- as well as non-financial matters such as:

- implications for the terms and structure of your customer contracts, and

- internal reporting and data capture systems.

If you haven’t yet started the implementation process, it’s 10 minutes to midnight and the clock is ticking. It is important to begin a diagnostic process to examine each of your key income types and contractual arrangements to assess where current accounting practice may change.

Failure to properly prepare and document your assessments may result in delays in finalising your 30 June financial statements and add additional audit time and costs.

Find out more

Nexia Edwards Marshall has published numerous articles, industry sector publications and webinars on applying the new revenue and income of not-for-profit entities standards. Contact Jamie Dreckow or your Nexia Edwards Marshall Adviser to discuss how we can assist you prepare for AASB 15.

The material contained in this publication is for general information purposes only and does not constitute professional advice or recommendation from Nexia Edwards Marshall. Regarding any situation or circumstance, specific professional advice should be sought on any particular matter by contacting your Nexia Edwards Marshall Adviser.