We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Jun 07, 2023 / News

Additional tax on super balances over $3 million

The Budget confirms the Federal Government’s intention (see Super Solutions Newsletter 16) to introduce an additional 15% tax on a proportion of the super “earnings” of a member where the member’s total super balance is greater than $3m at the end of a financial year. The new tax will be first levied in the 2025-26 financial year.

It is important to understand that this is not a flat 15% tax on “earnings”, but on a proportion of “earnings”, calculated as the proportion of total super balance (TSB) greater than $3m at the end of the financial year.

Perhaps the most controversial aspect of the new tax is that “Earnings” is not based on a fund’s taxable income, but is to be calculated using the formula:

Closing TSB – Opening TSB + Withdrawals – Contributions (net of contributions tax)

If the closing TSB is greater than $3m but the opening TSB is less than $3m, $3m is used as the opening figure to ensure that only balances over $3m will be caught in the tax.

As total super balance includes unrealised gains, these will be included in “earnings”, but there is still a great deal of uncertainty around precisely what will be included in “withdrawals” and “contributions”. For example, will the formula be adjusted to take account of the fund receiving a reversionary pension, insurance payouts for death or disability, or a payment split on the break-up of a relationship? Note also that TSB includes any retirement phase pensions, so “earnings” on these will be included in the new tax, even though the income on retirement phase pensions is exempt from ordinary income tax.

If an individual makes an earnings loss in a financial year, this will be able to be carried forward to reduce the tax liability in future years, but losses will not be able to be carried back to offset against gains of earlier years. Individuals will have the choice of either paying the tax out-of-pocket or from their superannuation funds. Of course, this raises the issue of whether the fund has sufficient cash reserves to pay the tax for the member.

The Federal Government has confirmed that the $3m threshold will not be indexed, and no new condition of release will be introduced to allow members to reduce their total super balances before the tax commences.

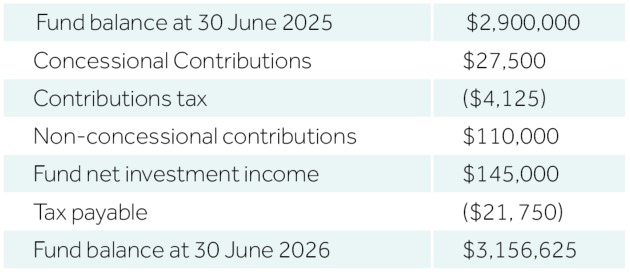

Example

Ron has only one super fund, so the balance in the fund is his total super balance. In the year ended 30 June 2026, the transactions in Ron’s super fund were:

The proportion of “earnings” subject to the tax would be:

(Closing TSB - $3 million) / Closing TSB, but $3m is used as the opening TSB because it was less than $3m:

($3,156,625 - $3,000,000) / $3,000,000 = 5.2208%

“Earnings” would be calculated as:

Closing TSB – Opening TSB + Withdrawals – Contributions (net of contributions tax):

$3,156,625 - $3,000,000 + 0 – ($27,500 - $4,125) -$110,000 = $23,250

And the amount of tax to be paid would be calculated as:

$23,250 x 5.2208% x 15% = $182.07.

In the year ended 30 June 2027, the transactions in Ron’s super fund were:

As Ron’s closing TSB is less than $3m, he will not pay tax in the 2026-27 year.

His fund “earnings” would be calculated as:

Closing TSB – Opening TSB + Withdrawals – Contributions (net of contributions tax)

$2,995,125 - $3,156,625 +0 – ($10,000 - $1,500) = ($170,000)

His negative fund earnings in 2026-07 can be carried forward and offset against positive earnings of later years, but cannot be carried back to obtain a refund of tax paid in 2025-26.

Even though the Federal Government has announced that the new tax will affect a small number of super fund members, the non-indexation of the $3m threshold guarantees that its impact will increase over time.

The change has been deliberately planned to commence after the next Federal election is due (in 2025). It is likely that the Federal Government will legislate the change now in order to allow it to campaign on the issue of “Better Targeted Superannuation Concessions” should the Opposition seek to repeal the tax.

Please contact your Nexia Edwards Marshall advisor if you wish to discuss this or any other superannuation issue.

The material contained in this publication is for general information purposes only and does not constitute professional advice or recommendation from Nexia Edwards Marshall. Regarding any situation or circumstance, specific professional advice should be sought on any particular matter by contacting your Nexia Edwards Marshall Adviser.