We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Oct 07, 2022 / News

ATO now contacting professionals about your profit allocation – are you prepared?

Lawyers, engineers, medical professionals, architects, financial advisors, accountants, and other professionals, if you are an equity-holder in your firm, you might soon receive a knock on the door from the ATO. Their sights are firmly targeted on the allocation of your profit share to lower-taxed related parties, such as your spouse, children and a corporate beneficiary.

Knowing where you stand is critical to making informed decisions – and you will need to make some decisions. And you’ll sleep better at night if you have already addressed this before the ATO knocks…

What’s the issue?

The ATO’s key concern is whether a sufficient amount of your profit share is taxed to you personally, reflecting the value of your personal efforts. In other words, is too much allocated to related parties on a lower tax rate? The ATO contends that this might offend certain anti-avoidance rules, and they have assembled a team for contacting professionals to enquire about your profit-allocation arrangements.

This follows from the ATO’s Practical Compliance Guideline PCG 2021/4: Allocation of professional firm profits, which sets out their approach to tax compliance for owners of professional firms. It applies from the current 2022-23 income year.

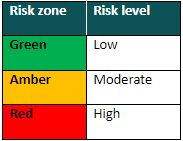

Targeting system for reviews

The PCG sets out a year-by-year scoring system which places you in one of the following risk levels:

Essentially, it’s a targeting system for determining whether the ATO will conduct a review of your tax arrangements, or leave you alone. There are several factors that determine your risk level for a year, and they are complex to process, as they involve a number components, adjustments and rules. However, the fundamentals are that the greater the proportion of your profit share taxed to you (and thus a lesser proportion to related parties), and the higher overall effective tax rate on your profit share, the greater likelihood of falling into the Green zone.

The ATO will generally leave you alone where you fall into the Green zone. Where you fall into the Amber zone, the ATO is likely to conduct a review. If you fall into the Red zone, the ATO firmly states that they will conduct a review of your tax arrangements.

ATO’s goal – find a test case

The fundamental difficulty with this profit-allocation issue is that the tax laws do not address it, and it has never been before the courts. Accordingly, there is no benchmark metric for determining exactly how much, if any, of your profit share ought to be taxed to you personally.

The ATO is searching for a suitable taxpayer to run a test case, to establish some kind benchmark metric. Obviously, you wouldn’t want to be that taxpayer. While putting yourself in the Green zone might leave you out of contention, that peace-of-mind will likely come with a higher tax cost.

Tax cost of moving to the Green zone

It has become apparent that, in most cases, a business-as-usual profit allocation will place you in the Amber or Red zones. The question then is how much extra tax you are prepared to pay for the peace-of-mind of a Green zone free pass.

We have developed a sophisticated calculator tool that we use to determine the zone into which your business-as-usual profit allocation will place you, and the tax cost of moving to the Green zone. When that extra tax cost is quantified, then there’s a discussion to be had, and only then can you make an informed decision – go to Green, or stay in Amber/Red.

Learn more, and what to do, at our session on Tuesday 15 November. For details and to register, click here. We look forward to seeing you there!

The material contained in this publication is for general information purposes only and does not constitute professional advice or recommendation from Nexia Edwards Marshall. Regarding any situation or circumstance, specific professional advice should be sought on any particular matter by contacting your Nexia Edwards Marshall Adviser.