We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Aug 13, 2019 / News

Financial Reporting Developments

Large/small proprietary company thresholds

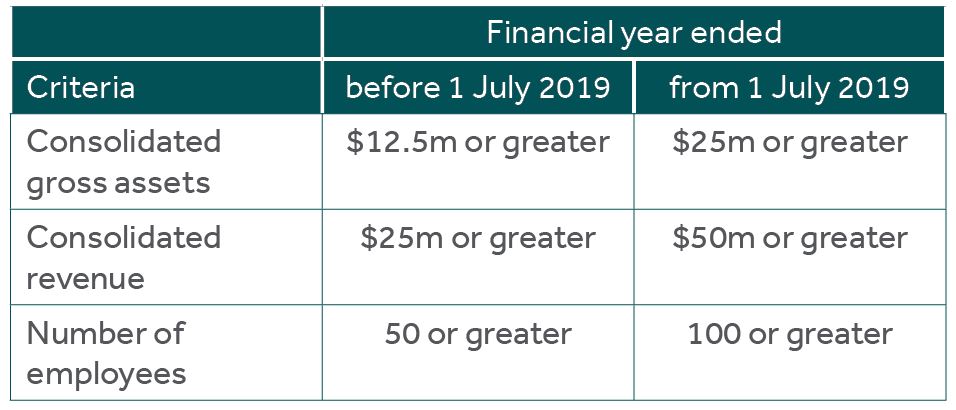

The thresholds for determining what constitutes a large proprietary company under the Corporations Act 2001 has been doubled effective for financial years beginning on or after 1 July 2019.

Companies that meet the criteria as a large proprietary company are required to prepare and lodge an audited financial report, a director’s report and an auditor’s report with ASIC each financial year.

A proprietary company is large if it satisfies any two or more of the following tests:

Increasing the thresholds will also change whether a foreign controlled proprietary company is assessed as large or small. These changes are significant as it will reduce the number of proprietary companies that are required to report under the Corporations Act 2001 and will also have implications on the Australian Accounting Standards Board’s (“AASB”) proposals regarding the removal of Special Purpose Financial Reports (“SPFR”) discussed below. It also pre-empts the government’s response to the recommendations from Treasury’s Legislative Review of the Australian Charities and Not-for-Profit Commission Act 2012 regarding financial reporting thresholds and financial statement requirements for registered charities.

Removal of Special Purpose Financial Statements

The AASB is proceeding with its project to prevent for-profit private sector entities that are required by legislation to prepare financial statements in accordance with Australian Accounting Standards from preparing Special Purpose Financial Statements (“SPFS”).

The initial stage of the Board’s project is focussed on for-profit entities and would primarily affect companies incorporated under the Corporations Act 2001. Other for-profit entities required by governing legislation to prepare financial statements in accordance with accounting standards would also be affected. The proposed implementation date for these changes is 1 July 2020.

In addition, these changes would apply to other for-profit entities that are only required by their constituting document or another document to comply with Australian Accounting Standards, but only where the relevant document was created or amended on or after 1 July 2020.

How we see it

For-profit entities such as small proprietary companies, trusts and partnerships that have constituting documents, or documents such as lending agreements, that require compliance with Australian Accounting Standards will not be required to prepare General Purpose Financial Statements (“GPFS”) provided such document or requirement existed before 1 July 2020.

However, if such constituting document or other document is created or amended on or after 1 July 2020 the exemption will no longer apply.

For example, Company A, a for-profit small proprietary company, obtained a bank loan during 2018. A condition of the loan requires Company A to prepare and submit annual financial statements prepared in accordance with accounting standards.

Company A is subject only to the Corporations Act 2001 and, as a small proprietary company, is not required by legislation to prepare financial statements in accordance with accounting standards. Consequently, Company A will not be required to prepare GPFS under that criteria.

Company A’s borrowing agreement contains a requirement to provide the lender its annual financial statements prepared in accordance with accounting standards.

However, because this condition existed before 1 July 2020, Company A is permitted to prepare a SPFS, provided this meets the information needs of its users.

However, if Company A entered into the same loan agreement on or after 1 July 2020, or if Company A’s existing loan facility were amended or renegotiated on or after that date, Company A would be required to prepare GPFS.

The AASB is still proposing two tiers of GPFS: Tier 1 GPFS which comply with the full measurement, recognition and disclosure requirements of Accounting Standards; and a revised Tier 2 which will contain the same recognition and measurement requirements as Tier 1 but would replace the existing RDR disclosure requirements with those based on the disclosures in the IFRS for SMEs standard.

At the present time, the above proposals will only impact for-profit entities. The AASB will separately turn its attention to not-for-profit entities once it has finalised its revised reporting requirements for for-profit entities. However, we don’t expect that the future changes for not-for-profit entities will be substantially different to those proposed above. The AASB has not confirmed an application date for changes for not-for-profit entities, but it is likely to be 12 months after the changes take effect for for-profit entities.

Changes to Business Combination accounting

The AASB has amended AASB 3 Business Combinations to provide more guidance on the definition of a business and to assist entities determine whether a transaction should be accounted for as a business combination or as an asset acquisition. It narrows the definitions of a business and adds an optional concentration test that permits a simplified assessment of whether an acquired set of activities and assets is not a business.

The amendments should make it simpler to assess whether an acquisition is a business combination or an asset acquisition. The amendment mandatorily applies from 1 January 2020 but it can be early adopted.

ASIC focus areas

ASIC has released details of its focus areas for 30 June 2019 financial reports.

Full-year GPFS at 30 June 2019 must comply with new accounting standards on revenue recognition and financial instruments and ASIC will be focussing on measurement and disclosures relating to these new standards.

ASIC also expects that 30 June 2019 financial statements will disclose the impact of the new lease accounting requirements which take effect from 1 July 2019.

Other areas of focus include:

- Impairment testing and asset values;

- The treatment of off-balance sheet arrangements and consolidation accounting;

- Income tax accounting, including recoverability assessments of deferred tax assets; and

- Disclosures regarding sources of estimation uncertainty and significant judgements in applying accounting policies.

Are you ready for AASB 16 Leases?

The new leases accounting standard, AASB 16, applies for financial years beginning on or after 1 January 2019. Bringing operating leases on to the lessee’s balance sheet is likely to have the most far-reaching effect on entities since the introduction of IFRS in Australia in 2005.

We can assist you prepare for AASB 16 by undertaking transition impact assessments, technical accounting advice and on-going lease accounting assistance. To find out more contact Jamie Dreckow, jdreckow@nexiaem.com.au

The material contained in this publication is for general information purposes only and does not constitute professional advice or recommendation from Nexia Edwards Marshall. Regarding any situation or circumstance, specific professional advice should be sought on any particular matter by contacting your Nexia Edwards Marshall Adviser.