We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Apr 23, 2020 / News

Not-for-Profit Newsletter - April 2020

Welcome to the newest edition of our Not-for-Profit Newsletter. Please feel free to contact us if you have any questions about the content of this Newsletter.

The current climate has tested many organisations and we understand that many of you may need assistance navigating your way through the changes. We encourage all of our clients to reach out to their Nexia Edwards Marshall Advisor so that we can assist you during this time.

In this edition

This edition covers the ACNC’s response to the COVID-19 pandemic that include compliance changes, a lodgement extension for 2019 Annual Information Statements, and a reminder of the importance of regular communication if a charity’s activities or plans have changed. The impact of current events on financial reporting and the application of the going concern basis is also discussed.

We have also highlighted some important changes for charities that prepare special purpose financial statements. The new requirements are applicable to the financial statements for the year ending 30 June 2020. This edition also includes an outline of the upcoming ACNC review of deductible gift recipients and a number of governance-related items including board remuneration and a reminder of the whistleblowing policy requirements.

Click on one of the Newsletter sections below to scroll to the section: ACNC activities / Financial reporting insights / Governance

ACNC activities

Charity operations in COVID-19 environment

Many charities’ operations are affected by COVID-19. This may mean that some or all of your charity’s activities may need to be modified or even temporarily halted.

The ACNC stated that is important for charities to keep everyone informed of what it is doing, and why. Regular communication about a charity’s changed activities should be a priority.

The commission stressed if your charity’s operations do change, it is important it remains consistent with its charitable purpose – what it was set up to achieve.

The ACNC has advised also that each charity needs to consider the financial effects.

They include:

- Considering the use of reserves

- Assessing their eligibility for the federal state or territory stimulus packages

- Considering any other financial assistance available (for example, business relief packages from banks or financial institutions)

- Assessing future cash flows and doing a forecast – or adjusting their forecast – in light of current events.

- Speaking to funders about the effects of cancelling or delaying activities that are part of funding agreements

- Knowing fixed costs and when they will need to be paid. Not committing to any more expenditure if possible

- Reviewing existing liabilities (for example, exploring options with banks or financial institutions, including deferring loan repayments if applicable).

Responsible Persons should speak to their charity’s accountant and auditor in preparation of budgets, forecasts and financial statements.

For a charity that has decided to cancel or postpone a fundraising event, there may be questions raised over what to do with any money already committed (for example, through ticket sales or other purchases).

For example:

- Will the money be refunded – either immediately or in time?

- Will the charity hold the money until the fundraiser is rescheduled?

- Will the charity commit the money towards a future event or effort?

The ACNC stressed that it important that a charity is transparent about what it is going to do.

It is important that it communicates clearly with supporters and other stakeholders the reasons why it made the decision, as well as the measures it has in place to ensure the funds are properly refunded or used in line with donors’ original intent and the charity’s charitable purpose.

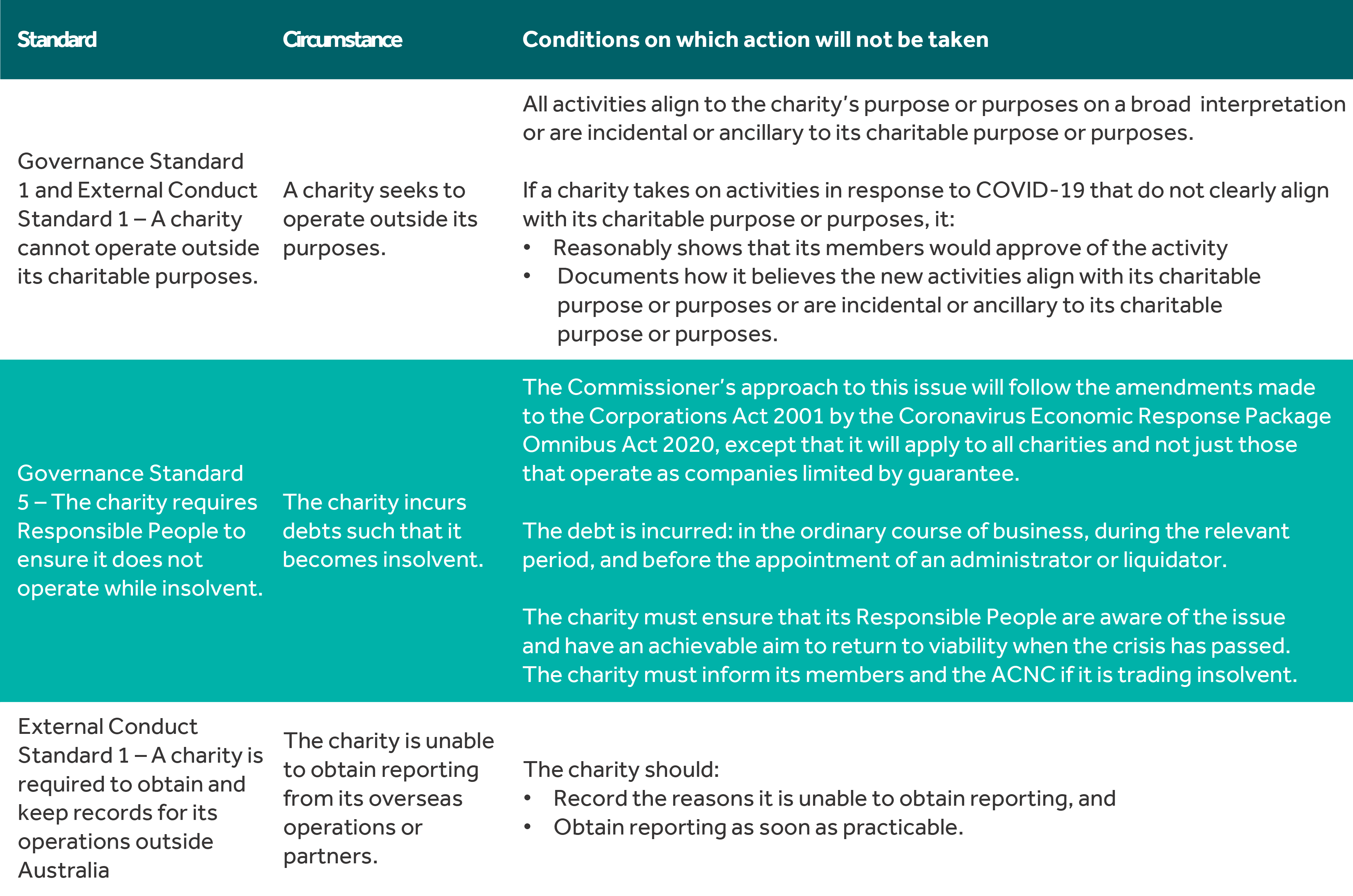

Compliance changes in response to COVID-19

In recognition of the unique challenges brought about by COVID-19, the ACNC has decided that the ACNC will not investigate certain breaches of the Governance Standards and the External Conduct Standards that occur from 25 March until 25 September 2020.

This approach is explained below.

The ACNC believes this short-term position is appropriate to allow charities to operate effectively and to enhance public trust and confidence in the sector.

If the ACNC identifies significant breaches that harm the public interest, even if it involves activities related to COVID-19, the commission may still investigate the issue and take regulatory action.

Annual Information Statement extensions

The ACNC Commissioner granted a blanket extension to charities with a 2019 Annual Information Statement due between 12 March and 30 August 2020. These charities will now need to submit their AIS by 31 August 2020. This advice will be monitored as the COVID-19 crisis progresses.

Insights into reporting statistics

Each year, the ACNC analyses a proportion of each of Annual Information Statement and financial reports to test the integrity of the data provided, and where necessary seeks corrections to errors.

The ACNC has released a report Reporting statistics for the 2018 reporting period which described major reporting statistics identified from its 2018 Annual Information Statement and Annual Financial Report (AFR) review process – including the most common errors found.

Key findings included:

- 68 per cent of charities selected the correct type of financial report to submit with their AIS. Of the remainder, the most common errors were the misclassification of General Purpose Financial Statements-Reduced Disclosure Requirement and Special Purpose Financial Statements as General Purpose Financial Statements

- 21 per cent incorrectly stated they were using transitional reporting arrangements – where the ACNC accepts financial reports prepared for and submitted to other regulators. These charities stated that they had to report to another regulator when in fact there was a streamlined reporting arrangement in place with that regulator –their charity was only required to submit a financial report to the ACNC

- 17 per cent incorrectly identified their financial report as a consolidated financial report when it was, in fact, a single charity report

- 42 per cent of charities that submitted a consolidated financial report provided AIS income statement and balance sheet figures for the consolidated group as a whole rather than financial information on an individual charity basis

- 75 per cent of AFRs examined included a complete set of financial statements. Of the remaining 25 per cent, the most common missing financial statements were those covering the statement of changes in equity and cash flow statement

Some common disclosure issues were: no disclosure on whether the charity was a for-profit or not-for-profit entity for financial reporting purposes; and the legislative framework under which the financial report was prepared did not mention compliance with the ACNC Act.

The commission will continue to review AFRs that charities submit to ensure compliance with the ACNC reporting requirements. It will also focus on ensuring that the financial information charities provide matches the information in their AFRs.

500 charities to undergo DGR review

Charities with deductible gift recipient endorsement are being encouraged by the ACNC to check their registration details, ahead of its reviews commencing in July 2020. The reviews are part of DGR reforms announced by the Government in 2017.

The DGR review is designed to strengthen the DGR governance arrangements and bolster confidence in the sector by ensuring that tax concessions are only held by eligible charities, that the integrity of the ACNC register is protected and donors have confidence that donations are applied to a charitable purpose.

Approximately 500 charities will be reviewed by the ACNC per year to assess if they are still eligible to be registered with the ACNC as a charity and subtype of charity and for DGR status. The initial focus will be on Public Benevolent Institutions.

PBI are the largest section of the DGR population (approximately 11,000), they can access the highest rate of tax concessions and, because they service such a diverse section of the community, have a substantial impact on trust and confidence within the sector.

PBIs will be identified for review based on a risk profile, which will include that they: were registered as a charity and PBI prior to 3 December 2012, are not regulated by the Office of the Registrar of Indigenous Corporation, have no, or only one Responsible Person listed or no governing document.

‘We will conduct reviews of 500 Public Benevolent Institutions that match our risk profile, but there should be no impact on charities under review, unless an issue is identified,’ ACNC Commissioner Hon Dr Gary Johns said.

In line with its commitment to transparency and education, and to ensure procedural fairness, the ACNC is encouraging charities to self-assess, using an online tool available on the ACNC website.

‘By using our self-assessment tool, charities will be able to identify and rectify most issues, such as nominating Responsible Persons and uploading their governing document to the Register,’ Dr Johns said.

‘Charities don’t need to notify us of those changes or send us their self-assessment. They can make changes easily through the ACNC Charity Portal.’

‘To promote good practice, we encourage charities to assess themselves periodically,’ said Dr Johns.

The importance of good governance

The bushfire crisis has seen an unprecedented amount of donations made to a range of not-for-profit organisations. As a result, the need for good governance and record-keeping practices are as important as ever stressed the ATO.

You need to make sure your NFP is operating for purpose. If your organisation is a DGR, you can only use tax-deductible gifts for the purpose of the DGR category you are endorsed under.

You must also keep records relevant to your organisation’s status as a DGR. Your records must show that all gifts and deductible contributions are being used for your principal DGR purpose.

Good records help you manage your obligations and make it easier to report and pay on time. Some of the basic records you may need to keep include:

- Governing documents

- Financial reports and operational records

- Tax invoices and income tax records

- Copies of reviews of entitlement to tax concessions, and

- Records to help prepare tax statements and returns.

Your records must be kept for five years and be in English, or easily converted to English. You should review your circumstances and entitlement to DGR endorsement regularly.

The Australian Charities and Not-for-profits Commission also has a number of useful resources for charities including the record-keeping checklist and self-evaluation checklist.

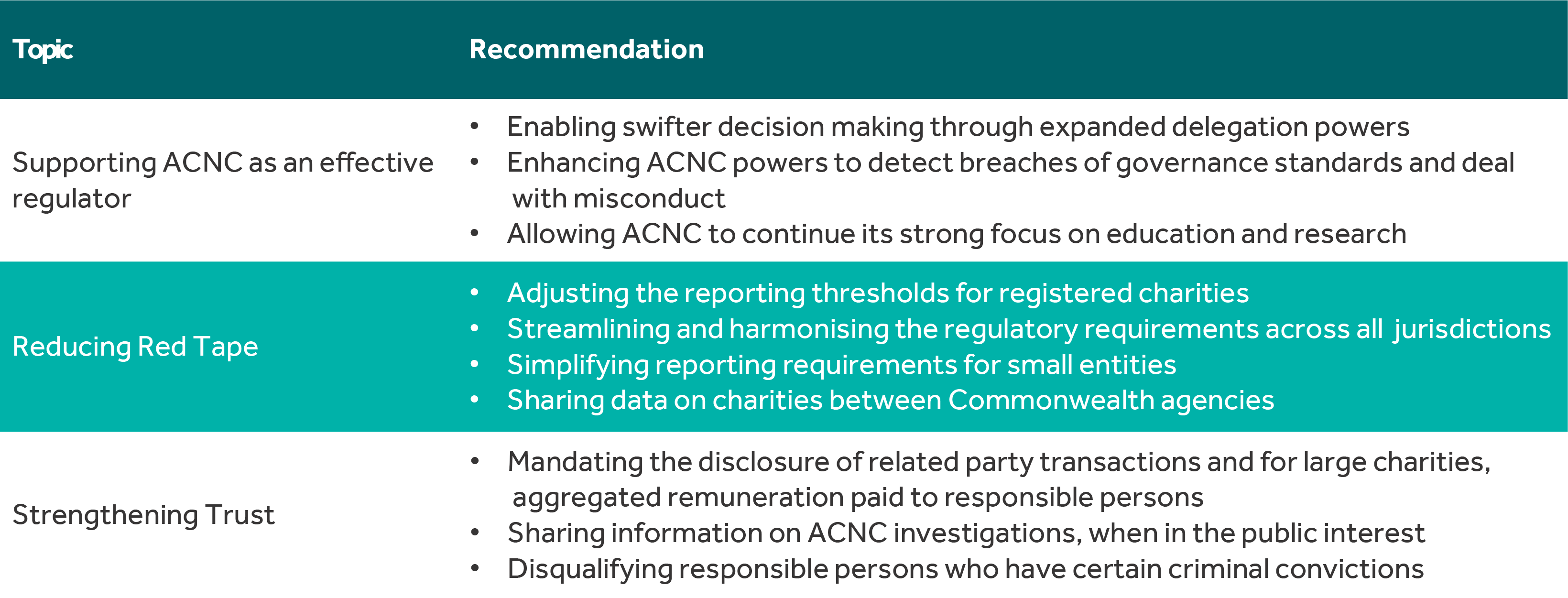

ACNC legislation review

The review report, Strengthening for Purpose: Australian Charities and Not-for-profits Commission Legislative Review 2018, made 30 recommendations, which centred on the ACNC’s objects, functions and powers, the overall regulatory framework, and red tape reduction for charities.

In its response to the ACNC Legislation Review, the federal government has responded to each of the 30 recommendations, agreeing with 18 of them.

The report is available to download here.

Financial reporting insights

COVID-19 financial reporting considerations

COVID-19 poses significant business risks that need to be effectively managed.

Unfortunately, major financial reporting and auditing consequences will follow the virus’s economic impact and social distancing. These need to be understood by boards and CFOs and processes put in place to deal with them. Such plans are unlikely to be set and forget.

Financial-reporting issues that immediately come to mind are the uncertainties associated with the going-concern basis of accounting, trigged impairment indicators for non-financial assets, impairment of financial assets under the expected-credit-loss model, changes to estimates and judgements, increased provisions, and more disclosures required in financial reports.

These will require extra attention in times of constrained resources and unavailability of staff.

Also, as business processes change due to strategies such as working from home, internal controls can be weakened, increasing the risks of non-compliance with laws, regulations, and fraud.

Act now to assess your financial reporting processes to minimise your risks.

Going concern revisited

AASB 101 Presentation of Financial Statements is the reference on going concern basis of accounting for preparers and will require much more consideration in the COVID-19 environment.

The rules are:

- When preparing financial statements, management must make an assessment of an entity’s ability to continue as a going concern

- The financial statements are prepared on a going concern basis unless management either intends to liquidate the entity or to cease trading, or has no realistic alternative but to do so, and

- When management is aware, in making its assessment, of material uncertainties related to events or conditions that may cast significant doubt upon the entity’s ability to continue as a going concern, the entity shall disclose those uncertainties.

- When an entity does not prepare financial statements on a going concern basis, it shall disclose that fact, together with the basis on which it prepared the financial statements and the reason why the entity is not regarded as a going concern.

In assessing whether the going concern basis is appropriate, management takes into account all available information about the future, which is at least but is not limited to, twelve months from the end of the reporting period.

The degree of consideration depends on the facts in each case.

Where there is a history and expectation of continued government funding and ready access to financial resources, management may reach a conclusion that the going concern basis is appropriate without detailed analysis.

In other cases, management may need to consider a wide range of factors relating to current and expected sources of income, debt repayment schedules and potential sources of replacement funding before it can satisfy itself that the going concern basis is appropriate.

In the current environment, management will need to have made a more detailed assessment of the suitability of the going concern basis than would have otherwise been the case. The disclosures in the financial statements will have to be more extensive, such a management plans to address the uncertainties with the application of the going concern basis.

New SPFS disclosures for 30 June

Under AASB 2019-4 Amendments to Australian Accounting Standards – Disclosure in Special Purpose Financial Statements of Not-for-Profit Private Sector Entities on Compliance with Recognition and Measurement Requirements, new disclosure requirements take effect for financial years ending on or after 30 June.

You will need to make new disclosures about your compliance with the recognition and measurement requirements in Australian Accounting Standards.

They apply to:

- Charities registered with the ACNC with an annual revenue of $250,000 or more and prepare special purpose financial statements, and

- NFP lodging SPFS with the ASIC under the Corporations Act 2001 (for example, companies limited by guarantee).

Your SPFS will need to disclose:

- Why the decision was made to prepare SPFS

- For each material accounting policy that does not comply with the recognition and measurement requirements, an indication of where it does not comply or that the assessment has not been made

- The overall compliance of your SPFS with the recognition and measurement requirements of accounting standards (except for consolidation and equity accounting), or whether this assessment has not been made, and

- Whether the consolidation and equity accounting requirements have been applied.

AASB 2019-4 makes amendments to AASB 1054 Australian Additional Disclosures.

FAQs on research grants updated

The AASB staff FAQs for not-for-profit entities on accounting for research grants have been updated.

The updates include:

- More Q&As

- Clarifying Scenario 1B on grants payable in instalments subject to agreed research activities being carried out, and

- Removing Scenario 2A, which has been included in the illustrative examples accompanying AASB 15.

Governance

Board remuneration considerations for NFPs

The Chartered Accountants Australia and New Zealand (CA ANZ) has released a business insight Remunerating Not-for-profit Directors covering key factors to be considered by not-for-profits in determining whether those charged with governance should be remunerated.

The paper includes a checklist highlighting aspects to be considered when contemplating remunerating Boards including an entity’s constitution, funding constraints, potential tax implications and other key agreements. A pros vs cons analysis for remunerating Boards is also outlined.

The case for remunerating Boards is centred around the need to attract a skilled and diverse group of individuals and provide recognition for their time and effort.

The argument for not remunerating those charged with governance is focused around the fact that it reduces the potential liability risks associated with being a director and it may also be perceived as being against the spirit of the sector, based on a belief that all of an NFP’s available resources should go directly to furthering the purpose of the organisation.

Download the paper from the CAANZ website here.

Whistleblowing policy reminder

Reminder public companies, amongst others, are required to have a whistleblower policy and to have made it available to their officers and employees by 1 January 2020.

Large charities that are companies limited by guarantee will need to have a Whistleblower Protection Policy which meets the requirements set out in the Corporations Act.

Small and medium charities that are companies limited by guarantee are exempt from meeting the requirement to have a whistleblower policy but are required to manage whistleblowing in accordance with the Corporations Act.

Finalised ruling – ‘In Australia’ condition

Taxation Ruling TR2019/6 Income tax: the ‘in Australia’ requirement for certain deductible gift recipients and income tax exempt entities has been issued. It sets out the Commissioner’s view on what the phrase ‘in Australia’ means where it is used in Divisions 30 and 50 of the Income Tax Assessment Act 1997.

Those Divisions set out rules for working out whether certain funds, authorities and institutions are eligible to be Deductible Gift Recipients and whether the income of certain NFPs is tax exempt.

The DGR ‘in Australia’ condition refers to the special condition that NFPs must be in Australia to be entitled to DGR endorsement. The ruling provides examples of when an entity: is established or legally recognised in Australia, and makes operational or strategic decisions mainly in Australia.

The ‘in Australia’ condition for exempt entities refers to the special conditions that certain NFPs need to meet in order to be tax exempt. The ruling provides examples of how an entity: meets the physical presence requirement, and demonstrates that it incurs expenditure and pursues objectives principally in Australia.

The finalised ruling is consistent with the guidance published in Draft Taxation Ruling TR 2018/D1 in July 2018.

Helpful tools from the IIA

The Institute of Internal Auditors in Australia have issued the following publications:

- Procurement integrity

- 20 Critical Questions – What to ask yourself during a pandemic lockdown

- 20 Critical Questions – What directors should ask of business continuity, and

- 20 Critical Questions – What directors should ask of compliance.

These are available on their website here.

How can Nexia Edwards Marshall help you?

If you have any questions on how the above may apply to you please contact Jamie Dreckow or your Nexia Edwards Marshall specialist.

The material contained in this publication is for general information purposes only and does not constitute professional advice or recommendation from Nexia Edwards Marshall. Regarding any situation or circumstance, specific professional advice should be sought on any particular matter by contacting your Nexia Edwards Marshall Adviser.