We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Nov 22, 2022 / News

Proposed new Tier 3 NFP reporting framework

From 2022 for-profit entities required to lodge financial reports with regulators have to prepare either Tier 1 or Tier 2 general purpose financial statements. The AASB is intending to extend this requirement to not-for-profit entities (NFP), which would affect ACNC–registered charities, co-operatives, NFP companies limited by guarantee, and others. But before doing so, it has issued a Discussion Paper detailing a proposed new third tier of general purpose financial statements.

Why a third tier?

The AASB has conceded that the Tier 2 general purpose reporting requirements, which requires the application of all recognition and measurement requirements of accounting standards, are too onerous and are not proportionate for some smaller NFP entities.

The primary objective of Tier 3 reporting is to develop a simplified financial reporting model that balances cost and benefits for stakeholders of smaller NFP entities. Consequently, it proposes a number of simplified measurement, recognition and presentation requirements compared to Tier 2 general purpose accounts. The AASB is targeting Tier 3 reporting to smaller NFP entities with simpler operations, typically with revenue between $500,000 and $3 million.

The AASB isn’t currently intending to specify which NFPs may or may not apply Tier 3 – that will be up to state and other regulators to decide.

What does Tier 3 propose?

Simplified requirements are aimed at the types of transactions and balances smaller NFPs would commonly have. Consequently the AASB has not attempted to modify the requirements of every accounting standard. Where a matter is not specifically addressed within Tier 3, an entity would need to look at the measurement and recognition requirements of other accounting standards.

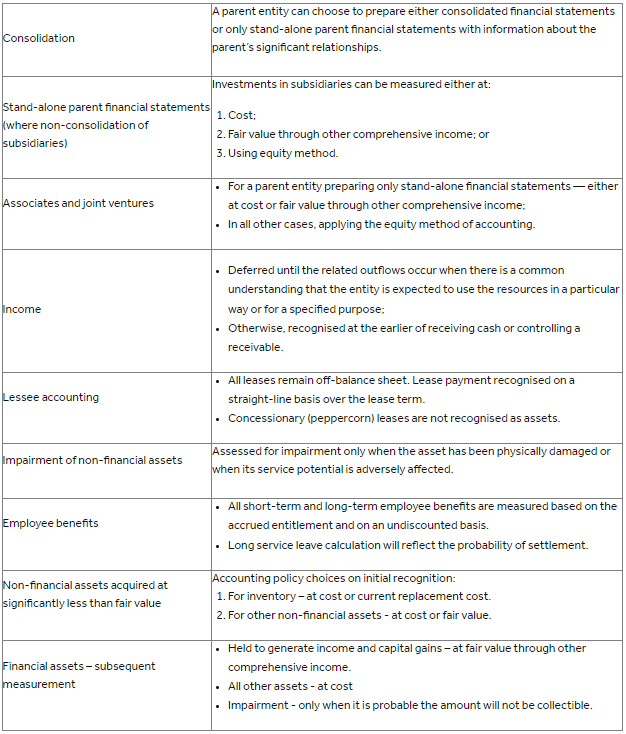

The Discussion Paper proposes the following key differences to Tier 1 and Tier 2 measurement and recognition requirements:

There are also a number of areas that the AASB has not expressed a firm view, such as how to transition between tiers and the extent of simplifying some disclosures.

In addition to the Discussion Paper the AASB has released a 12 page snapshot of the proposals and will be holding a series of virtual outreach sessions between November 2022 and March 2023 to gather feedback. You can find details through this link.

The AASB is open to developing a Tier 3 framework that is suitable and cost effective for smaller not-for-profit entities and is keen to receive feedback on its proposals. The Discussion Paper provides smaller not-for-profit entities a unique opportunity to help shape the direction of Tier 3 reporting without necessarily being tied to IFRS requirements.

The material contained in this publication is for general information purposes only and does not constitute professional advice or recommendation from Nexia Edwards Marshall. Regarding any situation or circumstance, specific professional advice should be sought on any particular matter by contacting your Nexia Edwards Marshall Adviser.