We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Jun 18, 2020 / News

Schools and Colleges Financial impacts of COVID-19

With evolving Government initiatives to assist businesses recover from any negative financial impacts of COVID-19, coupled with new financial risks, we have outlined below some key areas which may impact your School or College in 2020.

If you would like to better understand these impacts, we are able to offer a financial modelling service which considers the below and can provide better insight into your School’s or College’s financial position in this unprecedented time.

COVID-19-related Government grants

Several government stimulus initiatives in response to COVID-19 have been made available to many Schools and Colleges.

JobKeeper

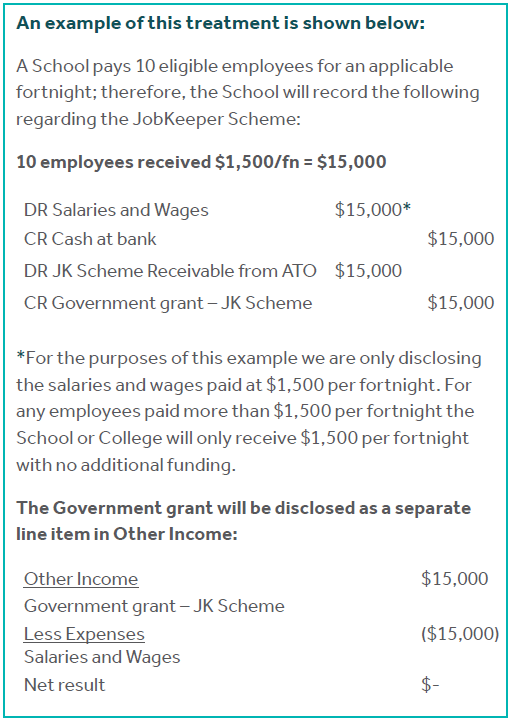

The JobKeeper payment scheme has been one of the initiatives that most Schools and Colleges have been considering. For accounting purposes this scheme is defined as a Government Grant.

JobKeeper government assistance is a temporary subsidy with eligibility criteria needing to be met to qualify for the payment, most notably the 30% reduction in turnover. This self-assessment requires appropriate record keeping and documentation to support your application and reported projected turnover calculations. This information will be an area of focus for your auditor (and the potentially the ATO) when considering compliance with the JobKeeper conditions.

The JobKeeper payments received are considered to be for the School or College and not directly for the employee. This is due to the School or College making the decision as to whether to apply for the scheme and taking on non-compliance risk by making payments to employees in advance of receiving any JobKeeper payments.

Therefore, these payments should be recognised by the School or College on a gross basis and not simply recorded through a clearing account (as if the School or College were acting as an agent) or as an offset to salaries and wages expense.

The School or College must also only recognise the revenue when they are satisfied that all conditions of the grant have been met (i.e. notably that the 30% reduction in turnover has occurred and the School or College has made payment to the eligible employees). If this is not the case, the grant should be recorded as a liability (unearned income) as the School or College may need to repay the grant due to non-compliance with the eligibility criteria.

AASB 1058 Income of Not-for-profit Entities will require that the JobKeeper payments be recognised immediately in profit or loss. The question arises as to when this immediate recognition is to occur; at the time of receiving payment from the ATO, or as a receivable at the time of the salaries and wages being paid to employees. Arguably, the School or College has self-assessed that it is eligible and the salaries and wages have been paid to employees for the period, and the School or College is therefore entitled to receive the cash from the government. Therefore, in our view it would be reasonable to recognise a receivable to the extent that the JobKeeper subsidy has not been received for the relevant month just passed. That said, we note that for many of you with December year ends this is largely a moot point as by 31 December 2020 all JobKeeper subsidies should have been received, assuming the subsidy is not extended beyond the current September 2020 deadline.

Leases

Schools and Colleges with leasing arrangements under AASB 16 that have received COVID-19-related rent concessions must consider whether they can access the optional short-term exemption which allows a potential lease modification to be treated as a variable lease payment.

To access the exemption, the following must be met:

- the concession must be linked directly to COVID-19;

- the change in lease payments results in revised consideration for the lease that is substantially the same as, or less than, the consideration for the lease immediately preceding the change; and

- any reduction in lease payments affects only payments originally due on or before 30 June 2021. (This has been extended from 2020 in the original proposal.)

It is important to note that if a rent reduction is negotiated and either part, or all of the reduction relates to post-30 June 2021, then relief is not available.

If a lease modification is required, then a remeasurement and adjustment will be required to the right of use asset and lease liability.

Any adjustment to the lease liability that is greater than the balance of the right of use asset will result in a gain and be credited to profit or loss.

Other areas for consideration during 2020

Whilst the impact of COVID-19 is constantly evolving on a daily basis, there are a number of areas that need to be considered as the year progresses and not just as part of the School’s or College’s year end processes.

Impairment (AASB 136)

Impairment of assets is something that should be considered at each year end. AASB136, Impairment of Assets, requires that when impairment indicators exist, a non-financial asset with a finite life must be assessed for impairment. Examples where indicators may be present in the School and College environment are where:

- government restrictions have rendered assets idle or where assets are no longer able to be used due to COVID-19 restrictions;

- there are plans to restructure the way the assets of the school are used; or

- there are plans to dispose of assets.

If you have concerns in the area of impairment, please contact your Nexia advisor for assistance with assessing the application of AAS 136 in making the decisions to write down assets.

Inventory (AASB 102)

Uniform shop inventory needs to be recorded at the lower of cost or net realisable value (NRV). It is possible that there may be some inventory that needs to be impaired due to certain co-curricular activities no longer being viable as a result of COVID-19 restrictions. There may also be slower moving inventory, which in turn results in an obsolescence issue, due to families no longer having the discretionary funds to spend on these items.

We recommend that Schools and Colleges review their inventory for items that are obsolete or where the NRV is less than cost.

Trade receivables (AASB 9)

Trade receivables is an area of risk for Schools and Colleges as parents / caregivers suffer the financial effects of COVID-19 job losses or reductions in income generally. The JobKeeper scheme may have assisted in deferring this impact somewhat, so we are expecting that the true effect of changes in family circumstances not to become fully apparent until the last quarter of the calendar year. We are aware that the initial round of COVID-19-related requests for fee concessions or bursaries have been significant for some Schools and Colleges, but this may be dwarfed by a potential second round later in 2020 going into 2021.

Employee Entitlements (AASB 119)

COVID-19 travel restrictions have put on hold the holiday plans of many employees and hence leave provisions may have increased somewhat as staff seek to bank their entitlements until restrictions alleviate. The management of leave provisions is often a difficult issue within schools, particularly those with long standing employees and COVID 19 may exacerbate a growing liability on the balance sheet.

Some measures you can consider implementing in your School or College are:

- forced annual leave for employees with excessive leave or in times of shutdown; or

- planned overseas travel to be altered to local intra state travel.

We suggest that Schools and Colleges revisit its leave policies to ensure they are relevant and appropriate given the current COVID-19 environment, this may include defining excessive leave for the School or College. If necessary an appropriately qualified HR expert should be engaged to assist with this.

Financial Modelling for the impacts of COVID-19

We have assisted several Schools and Colleges in developing financial modelling tools to ascertain trigger points to take appropriate measures to combat drop offs in student numbers. In these unprecedented times there are a number of assumptions that come into play with financial modelling and it is therefore important to have models that allow for flexibility and the ability to stress test potential scenarios.

We encourage any Schools and Colleges who need any assistance with this to contact Damien Pozza or your trusted Nexia Edwards Marshall Advisor.

How can Nexia Edwards Marshall help you?

If you have any questions on how the above may apply to your School or College, please contact Damien Pozza or your trusted Nexia Edwards Marshall Advisor.

The material contained in this publication is for general information purposes only and does not constitute professional advice or recommendation from Nexia Edwards Marshall. Regarding any situation or circumstance, specific professional advice should be sought on any particular matter by contacting your Nexia Edwards Marshall Adviser.