We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Feb 22, 2022 / News

(Almost) forgotten anti-avoidance rule is about to get your attention

Anti-avoidance shadow over trusts

For the vast majority of you, trusts would feature in your affairs. Accordingly, you need to be mindful every year of a number of anti-avoidance and integrity regimes, or at least your tax advisor needs to on your behalf. Since it was enacted over 40 years ago, section 100A of the Income Tax Assessment Act 1936 has cast a shadow over trusts, but hasn’t directly spooked the taxpayer community as much as it perhaps should have.

The reason for this could be that every case decision on this section – except the most recent one – involved promoted schemes. However, the ATO will soon release a ruling that will certainly demand our attention.

Narrow name, wide application

Perhaps another contributing factor to the limited attention given to section 100A over the years is the label the mischief being targeted ended up with – “Trust stripping”. It sounds like one of those notorious promoted tax-avoidance schemes from the 1970s – and that’s exactly what it was. However, even those who would never even consider such schemes could still find themselves falling foul of this anti-avoidance regime, with resulting exposure to higher tax bills, penalties and interest.

“Every-day” example of potential to offend s100A

The best way to explain the targeted tax mischief – and illustrate how section 100A can have a wide application – is by way of an example.

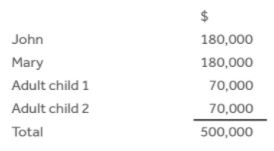

John and Mary have a family trust, which derives income from whatever source – perhaps they run a business through the trust, maybe it owns their share of a company, or perhaps it earns passive investment income. The trust has a net profit of $500,000 for the year, which is appointed to beneficiaries in the usual manner as follows:

By capping the appointed income to John and Mary at $180,000 each, they stay just inside the 39% marginal tax bracket, and thus don’t get into the top personal tax rate of 47%. Their adult children are at university, and each earns about $12,000 per year from a casual job. The $70,000 appointed to each of them therefore enjoys the remainder of the tax-free threshold, and the 21% and 34.5% tax brackets. The tax impost on the two lots of $70,000 is around $18,000 each – $36,000 in total. The trust pays out $18,000 on each child’s entitlement to cover their tax bill, leaving $52,000 owing to each.

All perfectly normal so far.

Now, how has the tax planning worked out? If the combined $140,000 appointed to the children had instead been appointed to John and/or Mary, it would have borne 47% tax – about $66,000. However, appointing it to the children bears only $36,000 tax, saving $30,000.

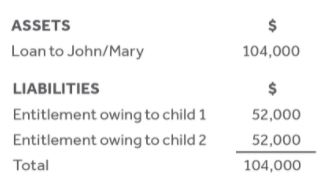

But here’s the thing. The trust still owes that remaining $52,000 each to the children. They are entitled to demand payment of the balance of their respective entitlement at any time. However, imagine there was an understanding with the children before appointing the income that they would not call upon their remaining profit entitlement. That means there is effectively an additional $104,000 ($52,000 x 2) available that John and Mary could take.

Once John and Mary have drawn funds from the trust such that their own $180,000 entitlement each is exhausted, what happens when they starting dipping into that $104,000? Typically, the trust is now making a loan to them – interest-free and with no repayment terms. The relevant parts of the trust’s balance sheet might ultimately look like this:

So, let’s recap. John and Mary appointed $140,000 of the trust’s profit to their children, paid down their entitlement by $36,000 to cover their tax bill, but there’s an understanding they won’t call upon any of their remaining $104,000. John and Mary then take those funds from the trust (as a loan) and use them for their own benefit. The bottom line is that John and Mary get their hands on income that was assessed to their children, and there’s an extra $30,000 in their pocket from the tax saving.

Sound too good to be true? It might well be.

Enter section 100A

The above situation could possibly fall within the anti-avoidance rules in section 100A. The reason is that the understanding between the parents and children might be regarded as a “reimbursement agreement”. This is just a label – no actual reimbursing of any kind is required. Broadly, a reimbursement agreement is where a trust appoints income to one person, but someone else gets the benefit of it, and there is a purpose of achieving a tax saving.

The effect of section 100A applying in the above example is that the trustee of the trust is assessed to tax on the $140,000 at 47% in place of the children’s original assessments. You might think that outcome is okay – if the ATO ever happened to conduct a review – as it would put John and Mary in the same position they would have been had the trust appointed the $140,000 to them in the first place, as they would have paid 47% tax in any case. However, there is the matter of penalty tax, which could be up to 50%, and the imposition of interest. Also, there is no time limit on issuing such assessments under section 100A.

There are any number of possible situations that could offend section 100A, but the fundamentals are the same:

- Trust appoints income to A (eg, someone on a lower income tax rate)

- Under an arrangement, by one means or another, B gets the benefit

- The overall tax impost on that income is less than it would have been, had the trust appointed that income to B

- The tax saving was the purpose of the arrangement.

Exception – ordinary family or commercial dealing

There is an exception to the application of section 100A, which is where the arrangement is entered into in the course of “ordinary family or commercial dealing”. Note that that is not saying the arrangement terms themselves must constitute such a dealing. Rather, the requirement is that the arrangement – whatever the terms are – came about from ordinary family or commercial dealing. In other words, what is done is not the issue; the issue is the process that gave rise to what was done.

It is likely easier to identity arrangements arising from “ordinary commercial dealing”, but there is uncertainty as to what constitutes “ordinary family dealing”.

ATO ruling pending

The ATO has been working on a long-anticipated ruling on section 100A, which is expected to be released soon. Rulings are not law; they are merely the ATO’s opinion. However, they often set out a good discussion of the subject and inform us on the ATO’s position on that subject.

The completion of the ruling was likely delayed due to the disruption caused by the COVID-19 pandemic. It might also have been further delayed due to the need to consider that abovementioned most recent case, Guardian AIT Pty Ltd v Commissioner of Taxation [2021]. In this case, it was determined that there was no reimbursement agreement in place, and what did occur was entered into in the course of ordinary family or commercial dealing in any case. The ATO has lodged an appeal against the decision, so that will likely delay the ruling even further.

When finalised, it is hoped that the ruling will provide practical guidance on where the ATO believes the line is drawn between circumstances that will and won’t offend section 100A. In particular, we are very keen to know their views on what constitutes “ordinary family or commercial dealing”. It is also hoped that the ATO will set out appropriate reasons and support for their views and where they draw that line.

We will certainly have more to say when a draft of the ruling is issued.