We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Mar 17, 2022 / News

ATO’s new regime for scrutinising your family trust

Anti-avoidance shadow over trusts

Each year, anyone with trusts in your affairs (or your tax advisor) needs to be mindful of a number of anti-avoidance and integrity regimes. Section 100A of the Income Tax Assessment Act 1936 has always cast a shadow over trusts, but has never received the level of attention it perhaps should have. The typical target scenario is this:

You appoint trust income on paper to a beneficiary on a lower tax rate, but someone else gets the benefit of the underlying funds

The ATO has now released a long-awaited draft ruling – TR 2022/D1 – setting out their views on where the line is drawn between acceptable and unacceptable practices in relation to the above. They have also released a draft Practical Compliance Guideline (PCG), which provides guidance on whose trust arrangements the ATO will investigate further, and whose they’ll leave alone.

Simple example of tax mischief

The best way to explain the targeted tax mischief is by way of a simple example:

- John and Mary are on the top personal tax rate of 47% (including Medicare levy)

- They have a family trust with income. They appoint $100,000 of trust income to their 19-year-old son, who has no other income

- The son’s tax liability on the above $100,000 (including Medicare levy) is about $25,000

- The trust pays the above tax bill, thus paying down $25,000 on the son’s entitlement. The trust still owes the remaining $75,000 to the son

- There is a largely unspoken understanding that the son won’t call upon that remaining $75,000 the trust owes him. This enables John and Mary to take the money and use it for their own purposes. This is reflected as a $75,000 loan by the trust to them

- The result is that the trust indefinitely owes $75,000 to the son, and the other side of that is the $75,000 loan to John and Mary

John and Mary could have simply appointed the $100,000 of trust income to themselves. However, they would have paid $47,000 in tax, leaving only $53,000 in their pocket. The above scenario instead leaves them with $75,000 to enjoy.

Sound too good to be true? It probably is.

Enter section 100A

The above situation and many others are squarely in the ATO’s sights for possibly falling foul of section 100A. The reason is that the understanding between John/Mary and their son might be regarded as a “reimbursement agreement”. This is just a label – no actual reimbursing of any kind is required. Broadly, a reimbursement agreement is where a trust appoints income to one person, but someone else gets the benefit of it, and there is a purpose of achieving a tax saving.

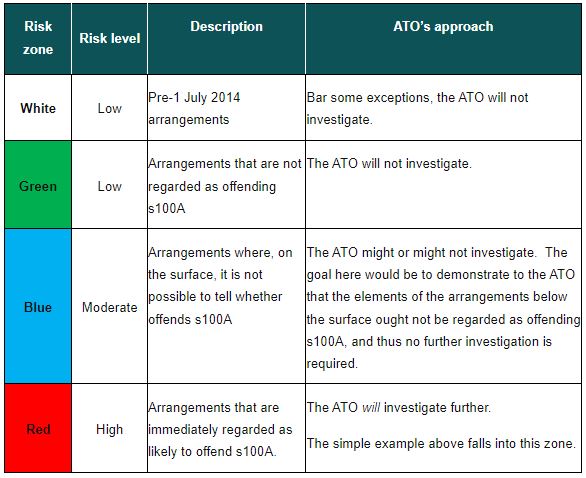

The abovementioned PCG sets out a zone system, to apply from the 2022-23 income year. Which zone your trust arrangements for any particular year fall into will determine the likelihood of the ATO investigating further. The PCG sets out a number of examples and guidance for when arrangements fall into the following zones:

Again, as noted, the draft PCG, which draws upon the draft ruling, sets out guidance and a number of examples of trust income appointment scenarios falling within each zone. Based on these, the John and Mary scenario above would fall into the red zone. The effect of section 100A applying in that scenario is that the trustee of the trust is assessed to tax on the $100,000 at 47% in place of the son’s original assessment. You might think that outcome is okay – if the ATO ever happened to conduct a review – as it would put John and Mary in the same position they would have been had they simply appointed the $100,000 to themselves in the first place. However, there is the matter of penalty tax, which could be up to 50%, and the imposition of interest. Also, there is no time limit on issuing such assessments under section 100A.

Circumstances described in a Taxpayer Alert will automatically fall into the red zone. The ATO has issued Taxpayer Alert TA 2022/1, which sets out scenarios similar to the example above.

There are any number of possible situations that could offend section 100A, but the fundamentals are the same:

- Trust appoints income to A (eg, someone on a lower income tax rate)

- Under an arrangement, by one means or another, B gets the benefit

- The overall tax impost on that income is less than it would have been, had the trust appointed that income to B

- The tax saving was the purpose of the arrangement.

Exception – ordinary family or commercial dealing

There is an exception to the application of section 100A, which is where the arrangement is entered into in the course of “ordinary family or commercial dealing”. Note that that is not saying the arrangement terms themselves must constitute such a dealing. Rather, the requirement is that the arrangement – whatever the terms are – came about from ordinary family or commercial dealing. In other words, what is done is not the issue; the issue is the process that gave rise to what was done.

In TR 2022/D1, the ATO discusses their views as to what constitutes an ordinary family or commercial dealing. The key feature is that it is “ordinary”. This reflects dealings as a whole that are capable of explanation as achieving normal familial or commercial ends. If that sounds a little wish-washy, it might help to know that a senior ATO officer once said that they use two specific tools when analysing these kinds of situations – the “sniff-o-meter” and the “excuse-a-scope”. There is merit in using these tools ourselves.

Recent case

The ATO issued the draft ruling despite a case examining section 100A currently before the courts, Guardian AIT Pty Ltd v Commissioner of Taxation [2021]. The Federal Court ruled that there was no reimbursement agreement in place, and what did occur was entered into in the course of ordinary family or commercial dealing in any case. The ATO has lodged an appeal against the decision. It would seem that the ATO would surely have to wait until this case is resolved before finalising the draft ruling.

Next step

We will continue to immerse ourselves in the draft ruling and PCG, and the final versions when released. For now, including the current income year, past practices and decisions of yours might require reassessment as to whether they continue to be appropriate. A prudent approach each year would be to make a judgement as to which of the above zones your proposed appointment of trust income would fall into. If the green zone, okay. If blue, the elements below the surface ought to be further considered against the section 100A criteria. If red, you need to be aware of the risk. Of course, the point of this exercise is to afford yourself the opportunity to consider a different income appointment decision.

Talk to your trusted Nexia Edwards Marshall advisor – we’ll certainly be talking to you in due course – about managing your trust income appointment decisions in light of these pronouncements from the ATO.

The material contained in this publication is for general information purposes only and does not constitute professional advice or recommendation from Nexia Edwards Marshall. Regarding any situation or circumstance, specific professional advice should be sought on any particular matter by contacting your Nexia Edwards Marshall Adviser.