We provide clients with many professional and technical services. For a detailed description, please select the relevant service.

Great

News

Mar 17, 2023 / News

FBT-exempt electric cars - For employers

As an employer, you are liable for Fringe Benefits Tax (FBT) on certain benefits provided to your employees and related parties. Some benefits are expressly exempt from FBT, and from 1 July 2022 that includes certain electric cars. This is now a differentiating factor when making decisions on acquiring cars in your business – petrol, electric or hybrid?

The following information will help you make these decisions in your business.

Who bears the FBT cost – you or your employee?

As an employer providing cars to employees, each car will generally fall into one of two categories:

- Your business bears any FBT liability

- Your employee bears any FBT cost as part of a salary-sacrifice arrangement.

The first category usually reflects circumstances where there is an inherent need for a car in order for an employee to carry out their duties. An example might be a travelling sales representative. In this case, the cost of providing a car – including any accompanying FBT – is a cost of business to you, the employer.

The other category is where an employee by agreement chooses to package a car into their remuneration under a salary-sacrifice arrangement. In this case, the employee sacrifices some remuneration in return for you the employer funding the costs of providing the car – again, including any accompanying FBT. In other words, with or without the car, your business’s total remuneration cost for that employee will be the same. The amount of each component (salary, superannuation, etc) will be different, but will add up to the same total.

Which cars are FBT exempt?

There are three key criteria for an electric car to be FBT exempt:

- The car was first “held and used” on or after 1 July 2022

- The car is a “zero or low emissions vehicle”, and

- The car’s retail price when sold new is below the luxury car tax threshold for fuel efficient vehicles.

A car might have been purchased new before 1 July 2022, but it will nonetheless meet the first criterion provided the first time it was used was on/after 1 July 2022.

A second-hand car can qualify, but only where it was first held and used by the original owner on/after 1 July 2022. Thus, no car first held and used before 1 July 2022 will ever qualify, either for the original or any subsequent owners.

A “zero or low emissions vehicle” is any of the following:

- Battery electric vehicle

- Hydrogen fuel cell electric vehicle

- Plug-in hybrid electric vehicle

All of the above vehicles have an electric motor for propulsion. In addition, a battery electric vehicle has neither a fuel cell nor an internal combustion engine. A hydrogen fuel cell electric vehicle also does not have an internal combustion engine, but does have a fuel cell for converting hydrogen to electricity. A plug-in hybrid electric vehicle includes an internal combustion engine for propulsion and/or generating electricity.

For plug-in hybrids, the exemption ceases on 1 April 2025. However, where you have a financially-binding commitment to continue providing a particular plug-in hybrid vehicle to an employee before that date, the vehicle will continue to be exempt for as long as that commitment remains in place. Once there is a change in ‘commitment’ post that date, the vehicle will no longer have access to the exemption.

The luxury car tax threshold for fuel efficient vehicles for the 2022-23 income year is $84,916 (including GST). A second-hand car will meet this criterion if its new-car price was below the threshold, irrespective of its second-hand price.

Providing your employee with a home charging station is not exempt. Also, as the exemption is only for “cars”, electric motor bikes and trucks are not included.

Illustrative scenarios

Your business bears the FBT

Where you provide a car that is in the first category above – that is, any FBT liability is a cost of business – there is a financial incentive to switch to an exempt electric car, as your business will simply save on the FBT cost no longer being incurred. For example, if you provide a $50,000 petrol car to an employee, including funding all running costs, your business will incur an annual FBT liability of up to around $10,000. However, if you instead provide an exempt electric car, you incur no FBT cost.

Your employee bears the FBT

For cars in the second category – that is, your employee chooses to package a car into their remuneration under a salary-sacrifice arrangement – the exemption provides no financial incentive for you. Rather, it is your employee who is motivated to choose an electric car. Whatever the components of your employee’s remuneration package (salary, superannuation, benefits, FBT, etc), they must total to the agreed remuneration package figure. So, with FBT now removed from the equation, the void is filled by additional salary and superannuation.

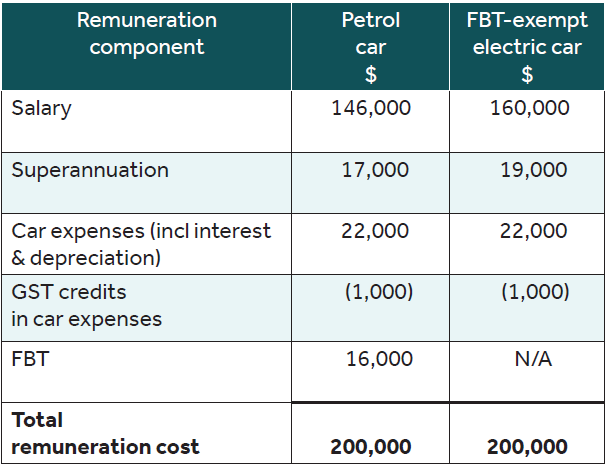

Here’s an illustrative comparison of an employee’s $200,000 remuneration package that includes providing an $80,000 car (figures are approximates):

In both cases, your business’s total remuneration cost is the same agreed package figure of $200,000. Yet, with the FBT-exempt electric car, the $16,000 FBT cost is replaced with approximately $14,000 additional salary and $2,000 additional superannuation. So, although your total remuneration cost remains the same, your employee has about an extra $8,500 in their pocket each year (ie, extra $14,000 salary, less 39 cents tax and Medicare levy) plus a little more superannuation.

It must be noted that the above does not take account of the fact that an electric car is generally more expensive than an equivalent petrol car. Thus, the $80,000 electric car will likely be smaller and/or have fewer features than the $80,000 petrol car.

Reportable fringe benefits

Although you incur no FBT liability when providing an exempt electric car to an employee, it remains a reportable fringe benefit. This means you need to notionally calculate the taxable value of the benefit as if it were subject to FBT. Accordingly, consideration ought to be given to whether maintaining a valid log book and tracking operating costs will result in a lower taxable value than the statutory method. The former entails greater administrative costs compared to the latter.

However, where the car is packaged under a salary-sacrifice arrangement like in the example above, you need to track operating costs in any case for measuring remuneration.

If the total notional taxable value of the car and certain other fringe benefits provided to the employee is greater than $2,000 for the year, the grossed-up taxable value figure must be disclosed on your employee’s annual payment summary. Alternatively, you can elect to notify reportable fringe benefits through Single Touch Payroll.

We can help

Talk to your trusted Nexia advisor about how we can help you make these decisions in the best interests of you, your business, and your employees.

The material contained in this publication is for general information purposes only and does not constitute professional advice or recommendation from Nexia Edwards Marshall. Regarding any situation or circumstance, specific professional advice should be sought on any particular matter by contacting your Nexia Edwards Marshall Adviser.